What "Working Capital Peg" Actually Means at the Closing Table

The number that quietly costs you $200K.

Most founders spend months obsessing over their EBITDA multiple. They negotiate the headline number, protect the earnout, argue over the seller note rate. Then they lose $200,000 in the final 72 hours of a deal not to the buyer’s attorneys, not to a surprise in due diligence, but to a clause they half-understood when they signed the LOI.

The working capital peg is one of the most consequential and least discussed mechanisms in a lower middle market acquisition. It is not a detail. It is a pricing lever and buyers know how to use it better than most sellers know how to defend against it.

The premise sounds reasonable enough: a business should be delivered with enough working capital to operate normally after closing. No stripping the balance sheet right before you hand over the keys. That’s fair. The problem is that “normal” is a number someone has to define and whoever defines it controls a significant portion of the final proceeds.

Understanding this mechanism isn’t optional for founders negotiating exits. It’s table stakes.

1. The Peg Is a Negotiated Number, Not an Objective Fact

The working capital peg is a target typically expressed as the trailing twelve-month average of net working capital (current assets minus current liabilities, excluding cash and debt). If the business delivers more working capital than the peg at close, the seller gets a dollar-for-dollar upward adjustment. If it delivers less, the buyer takes a dollar-for-dollar reduction.

Here’s what most sellers don’t realize: the peg itself is negotiated, not calculated. A buyer’s advisor will anchor to the highest defensible trailing average. A seller’s advisor will push for a methodology that reflects normalized operations, seasonality-adjusted. The difference between those two interpretations can easily be $150,000 to $300,000 on a $5M transaction.

Neither side is lying. They’re selecting the methodology that serves them.

💡 Rule: Treat the peg negotiation like price negotiation because it is. Agree on the calculation methodology before you agree on the number.

2. The Definition of “Working Capital” Is Not Standard

Current assets minus current liabilities sounds clean. In practice, the components are fought over line by line.

Does cash count? Usually excluded but how much minimum cash stays in the business? Are customer deposits current liabilities or deferred revenue? What about prepaid expenses, accrued bonuses, or that $80K equipment lease that’s technically current? These classifications are accounting judgment calls, and they move the peg in one direction or the other depending on who’s making them.

Sellers should walk into LOI negotiations with their own working capital model already built not waiting for the buyer to define the universe of included accounts. Whatever is excluded from the peg definition should be explicitly listed in the purchase agreement.

If you’re using Deal Flow OS to model your deal structure before you get to the table, the deal structure builder can help you map out working capital components and stress-test adjustment scenarios before your first call with a buyer’s accountant.

💡 Rule: Define the accounts included in working capital before you define the target. The inclusion list is where the real money moves.

3. Seasonality Can Destroy a Fair Peg

A business with significant seasonality retail, landscaping, tax services, anything with a fiscal cycle has wildly different working capital balances across the year. If the deal closes in October and the peg was set using an annual average that includes high-inventory summer months, the seller is almost certain to deliver a shortfall.

This is not a hypothetical. It’s a structural feature of how peg calculations work when buyers don’t make seasonality adjustments or choose not to. The right approach is to set the peg based on working capital expected at the time of close, adjusted for the business’s operating cycle. That requires the seller to present a credible methodology before the buyer’s QofE team presents theirs.

💡 Rule: If your business is seasonal, model working capital at the expected closing month specifically not as a trailing average across all twelve.

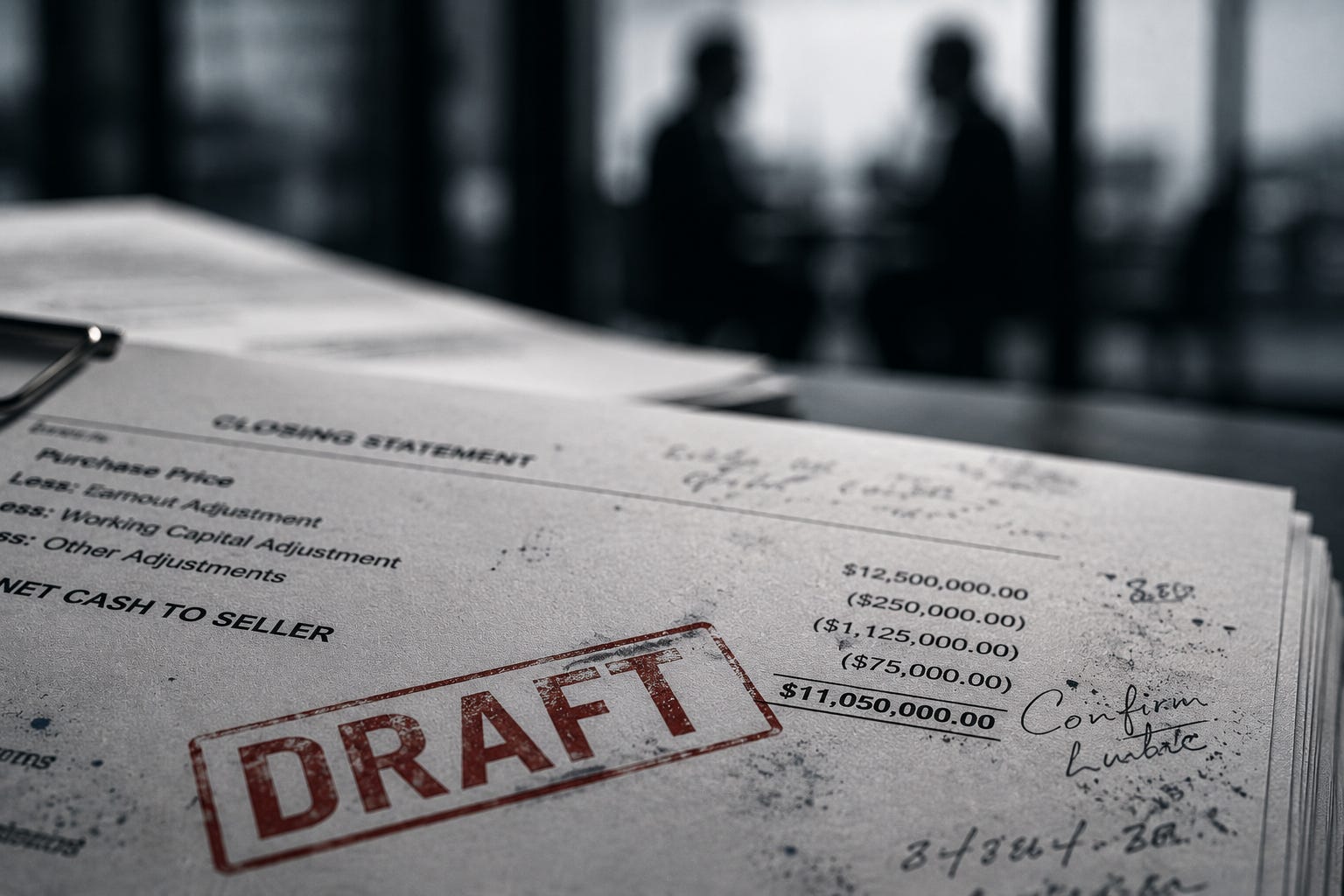

4. The True-Up Period Is Where Post-Close Losses Happen

In most deals, closing happens on an estimated working capital number. The final number and the adjustment is determined 60 to 90 days later, after the buyer’s accountants have completed a closing balance sheet audit.

Sellers frequently discover the adjustment is worse than expected during this window. Sometimes it’s legitimate receivables collected faster than expected, payables paid down before close. Sometimes it’s aggressive accounting by the buyer’s team, reclassifying items that were never in dispute during LOI negotiation.

The mechanism for contesting a post-close adjustment is usually an accountant dispute resolution process. But that takes time, costs money, and most sellers exhausted from a months-long deal process simply accept a number they shouldn’t.

Your protection is having a working capital accountant review the closing statement before the dispute window closes. Not after.

💡 Rule: Build a post-close review into your deal timeline. The 30-day window to contest a closing statement is not administrative it’s the last moment you have any leverage.

5. Sellers Who Understand the Mechanism Negotiate Better Floors and Collars

The working capital adjustment is theoretically uncapped in either direction. A seller can receive a meaningful upward adjustment or face a large reduction. Most buyers prefer this open-ended structure. Most sellers should not accept it.

The negotiating move is a collar: a band of $50,000 to $150,000 around the peg within which no adjustment is made. The adjustment only triggers outside that range. This protects both sides from noise in the final accounting and protects sellers from aggressive post-close reclassifications that fall just below a contestable threshold.

Collars are common in upper middle market transactions and underused in lower middle market deals, primarily because sellers don’t ask for them. Asking for one signals sophistication and often lands.

💡 Rule: Propose a collar in your initial markup of the purchase agreement. It’s easier to get it before the buyer’s counsel has drafted around an open-ended adjustment.

The Framework

Net Proceeds = Purchase Price ± (Actual WC at Close − Negotiated Peg)

Control the peg. Control the methodology. Control the timing. The adjustment isn’t incidental it’s the last repricing of your business.

Final Thought

The founders who lose money at the working capital adjustment didn’t lose it because they didn’t understand accounting. They lost it because they assumed the peg was a formality a back-of-envelope number that would roughly wash out. It rarely does.

If you’re modeling an exit, build the working capital analysis before you sign the LOI. If you’re a buyer, understand that a well-prepared seller has already done this math. The peg isn’t a surprise to them and it shouldn’t be to you.

Deal Flow OS gives both sides the tools to model deal mechanics, including working capital stress tests and net proceeds calculations, at dealflow-os.com.